“There is no inherent money neutrality, neutrality must be constructed by institutional arrangements. Much of the New Deal in the 1930s and 1940s was designed to build alternative channels for lending”

it’s the Cantillon effect, the closer to the mine, the first to spend the new coins and drive inflation against those farther away.

In current terms, it’s the central banks who are very good to discount bonds and inject liquidity into big corps, but there’s no one just as good in lending to homeowners, small businesses, workers etc.

So, in the big financial crisis, banks get bailed while homeowners are kicked out of their homes.

In Covid times, the government makes a multi.trillion rescue package and the stock market rally, because money gets more easily to listed companies.

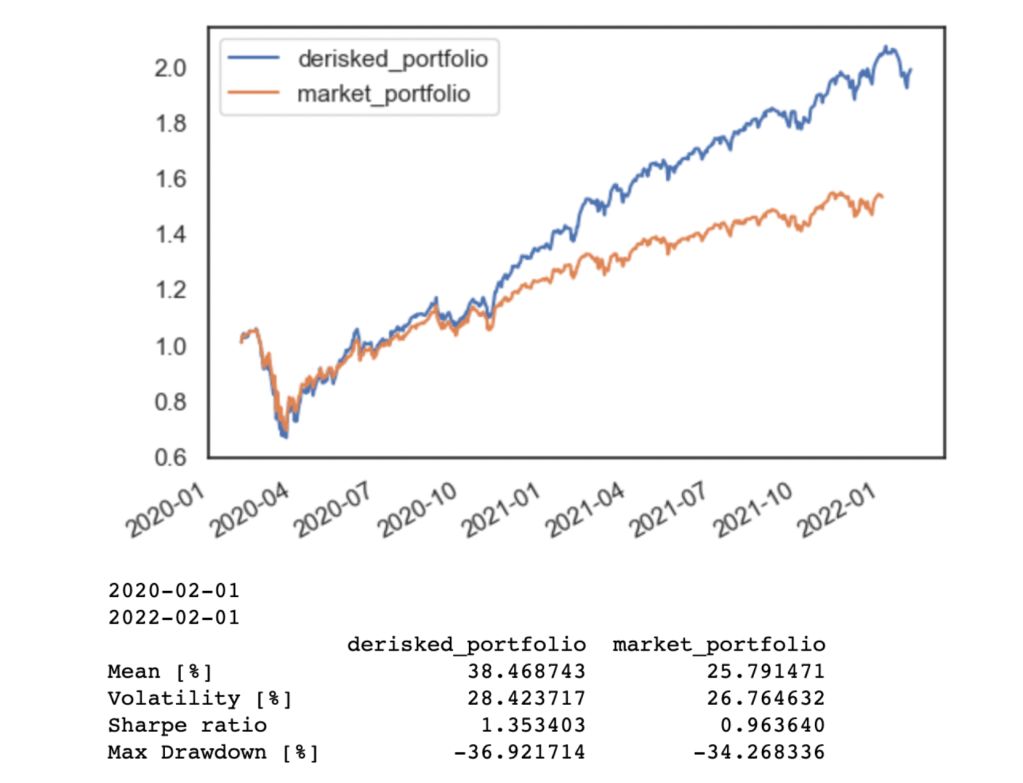

Policy Tensor notes that in stocks money is made at night, with markets closed

the post also mention “the strategy” how large hedge funds acted back then, trading at open where thier size can influence the market and then again at close when market is more liquid. This Knutsetson theory, he argued that “because markets are less liquid in the morning than they are in the afternoon, a hedge fund with a large portfolio can “expand his portfolio early in the day, when his trading moves prices more, and contract his portfolio later in the day, when his trading moves prices less, creating mark-to-market gains on his large existing book that exceed the cost of his daily round-trip trading.”

Anyway there’s more theory discussed but there’s also how to build a “derisked” portfolio on this idea of overnite gains, that would have performed wonders to date.

“Derisking” should have a mention here already, used by Daniela Gabor on Blackrock and climate investments, with a completely different meaning, and indeed “(just to piss off Daniela Gabor).” 🙂

se sei dall’altra parte, quella di ricevere un’offerta da una startup, a questo link puoi trovare dei riferimenti su quanto farti pagare quante opzioni chiedere a seconda dello stage della startup

nei tempi che viviamo non c’è più la netta differenza tra lavoro e capitale, tra lavoratore e imprenditore nell accesso a redditi da capitale, il modo migliore per affrontare la vita è quella di lavorare per avere delle quote di azioni del posto in cui lavori

Questo fenomeno di crescente sovrapposizione tra il ruolo di lavoratore e capitale, si definisce homoploutia. il termine è stato coniato dall’economista Branco milanovich ed è giusto conoscere il fenomeno per capire come funziona la distribuzione del reddito la disuguaglianza nel mondo attuale.

esci dalla facoltà di economia con l’idea che l’uomo economico è razionale e su questa razionalità l’economia non riesce a spiegare la cooperazione: l’uomo economico pensa solo a massimizzare la propria utilità e lo fa pensando a se stesso

poi, 30 anni dopo, scopri che questo è così per come la teoria dell’utilità è stata formalizzata a partire dal 18esimo secolo. Ogni decisione che l’attore razionale prende è autonoma da ogni altra, un attore razionale che fa molte scelte -per la teoria della utilità- lo sta facendo nei diversi universi di un multiverso. E’ la conseguenza di aver ipotizzato l’ergodicità, cioè l’omogeneità nel tempo per cui si può ipotizzare l’indipendenza degli eventi. Togliendo la storia dalla teoria ‘economia dell’utilità.

Invece se la storia la si rimette dentro, quello che decido oggi si “compund” su quello che ho deciso ieri e sarà la base del compound della decisione di domani, allora si ha una cosa come The Farmer Fable, dove il comportamento razionale, cioè quello che massimizza l’utilità, è la cooperazione e il pooling delle risorse. Potere del compounding dell’utilità, della storia invece del Multiverso

Questo nuovo approccio -in maniera poco chiara IMO- viene chiamato Ergodicity Economics, in realtà the economics che elimina l’assunto di ergodicità per arrivare a una descrizione piùrealistica dell’essere umano che investe e nel farlo elimina anche un po di paradossi che si sono presentati nella teoria tradizionale.

on the same day, BTC close to 50k USD and reading this in my inbox:

“getting money into the market was pretty hard. You need USDCoins, a stablecoin related to Ethereum. Polymarket tries to let you buy them directly, but their app wanted me to give them a security code which never showed up, so I gave up on this. Instead I bought some USDC at Coinbase and tried to send them over. But along with the usual Ethereum gas fees, they have something called a relayer, which is supposed to collect my money and put it in my account. And it’s apparently heavily backed up, and after two days my money is nowhere to be seen (though I believe them when they say that they’re trying their hardest and it will probably percolate through the Ethereum network someday). ” (that ws metaculus day on Astral Code, prediction market seems a perfdect application for blockchain)

but still the blockchain gold keeps climbing but useful applications seems nowhere to be found, at least for me who I’d be eager to move onto decetralized web.

But I would not quetion BTC value, and Dogecoin value. I had expected that this value would have unlocked a new web for us users but uktemately it unlocked new users in the traditional web.

The Coursera course in finance, the Nobel prize professor tells of Carnegie, the job of an investor is getting rich young and then devote to charity. This is a perfect sensible advise, a perfect acceptable career and it is probably what is going on the blockhains. BTC is the gold, hordes of hodlers pumped up on the same FOMO of social networks, The master of Twitter plays along.

so the value of an asset if the social construct of the beliefs held by the particpants to that market, blahblahblah but that’s the idea. If they had set to a finite number the banknotes in the mmonopoly game, the cardboard one, no digital and told you that if anough poeple bought it you could get rich and overturn the central banks. WoW could have done it. Well BTC is decentralized and better, though maybe Monopoly and Wow are more fun.

This is the great divergence, the price is there, is there some fun on the blockchain ?

I don’t know wether the cluster bomb model is appropriate, maybe a better analogy is the virus shedding, so IPO’s would be shedding capital in the economy, infectious innovation model

in Europe this does not happen and indeed the startup scene in Europe is sort of depressing, let alone Italy where it dead

going back to Branko Milanovic homoploutis, which he found increasing in the US, will it increase in the same way in Europe? The startup capital shedding model seems a big contributo though he does not mention it in his book, in his paper it is ecluded from the data but claerly reinforces the trend http://www.lisdatacenter.org/wps/liswps/806.pdf

It was 50 years from the day Friedman’s paper was published last september 2020, it took some time but by the early 80’s shareholder value took hold in the the corporate world, fuelled a rally in stocks and became one with the Reagan era

and this is the article, there an IPO that doubles immediately, there’s a six-month old partnership that is worth a 2-billion windfall, there’s a member of the paypal mafia

then in email I get one of those nice newsletters full of screen grabs, this is about the market piling up call otions, therefore being bullish above its means (and the dealers getting short gammma) from the dailyshot https://dailyshotbrief.com/the-daily-shot-brief-january-13th-2021/

Homoploutia is the situation where the same people (homo) are rich (ploutia) in terms of both labor and capital income. We measure it by the share of top decile capital-income earners who are also in the top decile of labor income.

First finding: Homoploutia has increased considerably since 1950, from about 10% to 30%, most notably in the past 35 years.

Second finding: The rising labor income inequality during the 1970s and 1980s fueled the increase in homoploutia. Either through higher saving leading to higher capital income, or higher incentives to participate in the labor force for the capital-income rich.

Third finding: in turn, rising homoploutia acted to increase (total) income inequality, accounting to 2 percentage points (or 20%) of the rising top 10% income share from 1986 to 2020. It may have played a bigger role in increasing US inequality than the capital share.

related, K shaped recovery in Coronatimes, where educated people with stock holdings are doing well, while no-degree workers in hospitality type works with no savings take the brunt of it all

also related, the growing importance of startups, unicorns etc which give options at early stages making both well paid and capital rich employes

The idea would be to teach pupils about savings, investments, taking and managing risks, using all the tools to buy and sell financial isntruments which are readily available today. The citizen investor, teaching kids to a better economic and financial position in the world.