still on the issue of the cancelled singularity

a dinner chat between a physicist and an economist on the physical limits to infinite growth , the infinite growth postulated by economists in their models.

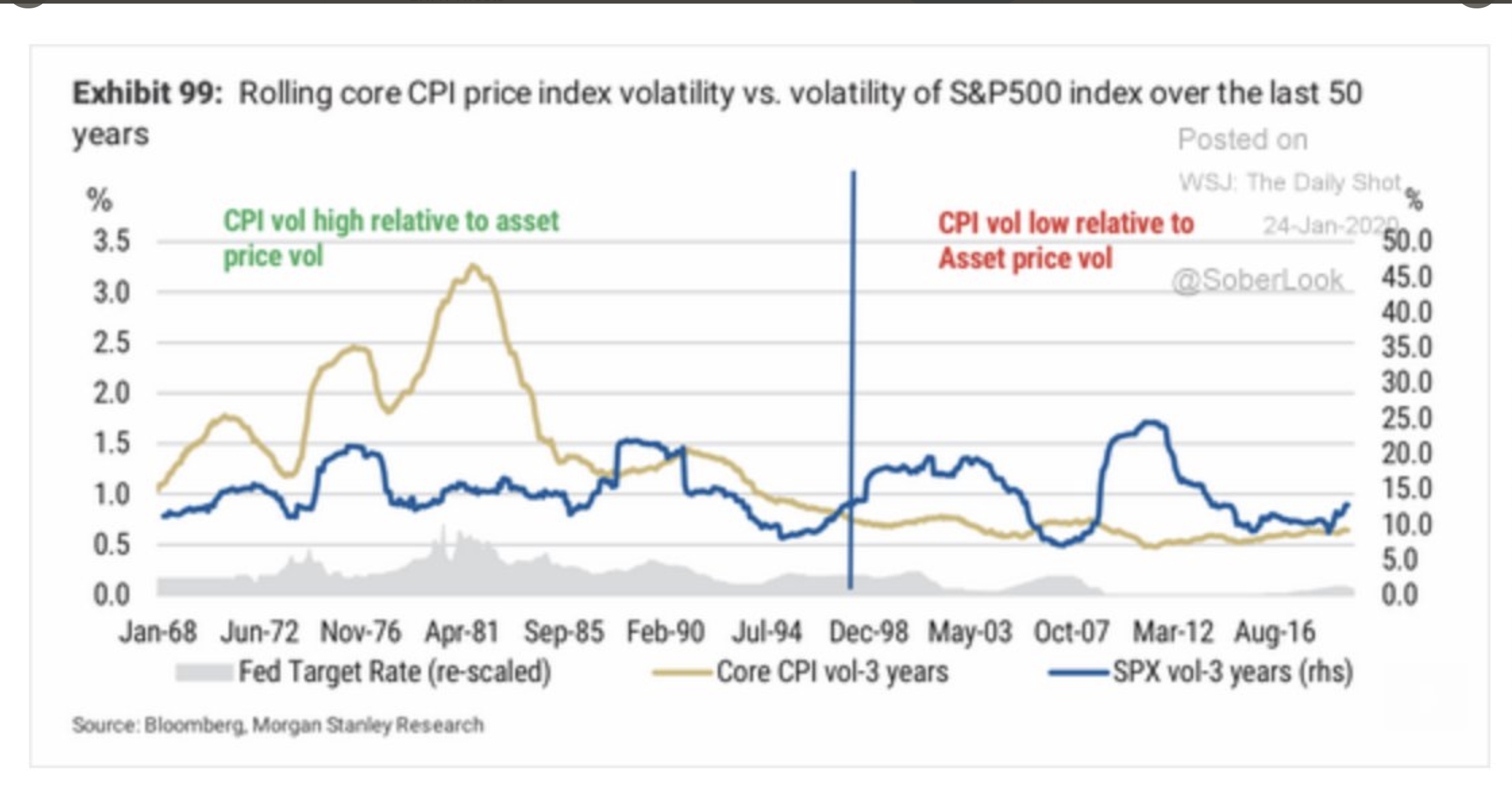

I got there from this tweet on ergodicity economics https://twitter.com/DrCirillo/status/1201782869712146432

and gave another read to Ole Peter’s Nature paper which sinks deeper in my reasoning on economics.

It all started because some economist on Facebook complained that some other economist had opposing views, but this is not the point, he started with an “in science, no economic theory …” science and economics so close in one sentence got me thinking about epistemics

a comprehensive article on “is economics a science?” lots of quotes so probably it isn’t you would not need so many instead

EDIT: I found today Noah Smith arguing that economic policy today seems limited to “Give poeple money” without any attempt to ground the directive in theory, unlike what happened in 2008 crisis where economists resorted to theory and in course they wrecked the economy even more. So the state of economics, macroeconomics I mean, is dismal https://noahpinion.substack.com/p/the-new-macro-give-people-money

UPDATE june2021:I had not realized that Noah Smith had a rebuttal of the physicts and economist dialogue https://noahpinion.substack.com/p/murphys-law-or-follies-of-a-finite